Too Late Powell

And the Future of the Fed

Jerome Powell’s tenure at the Federal Reserve will be remembered less for any single decision than for a pattern, delay followed by overcorrection, then delay again. The record matters because monetary policy is not judged on intent or rhetoric, it is judged on sequence, magnitude, and lag. When the lags are misread, the damage compounds quietly before it shows up loudly in the data.

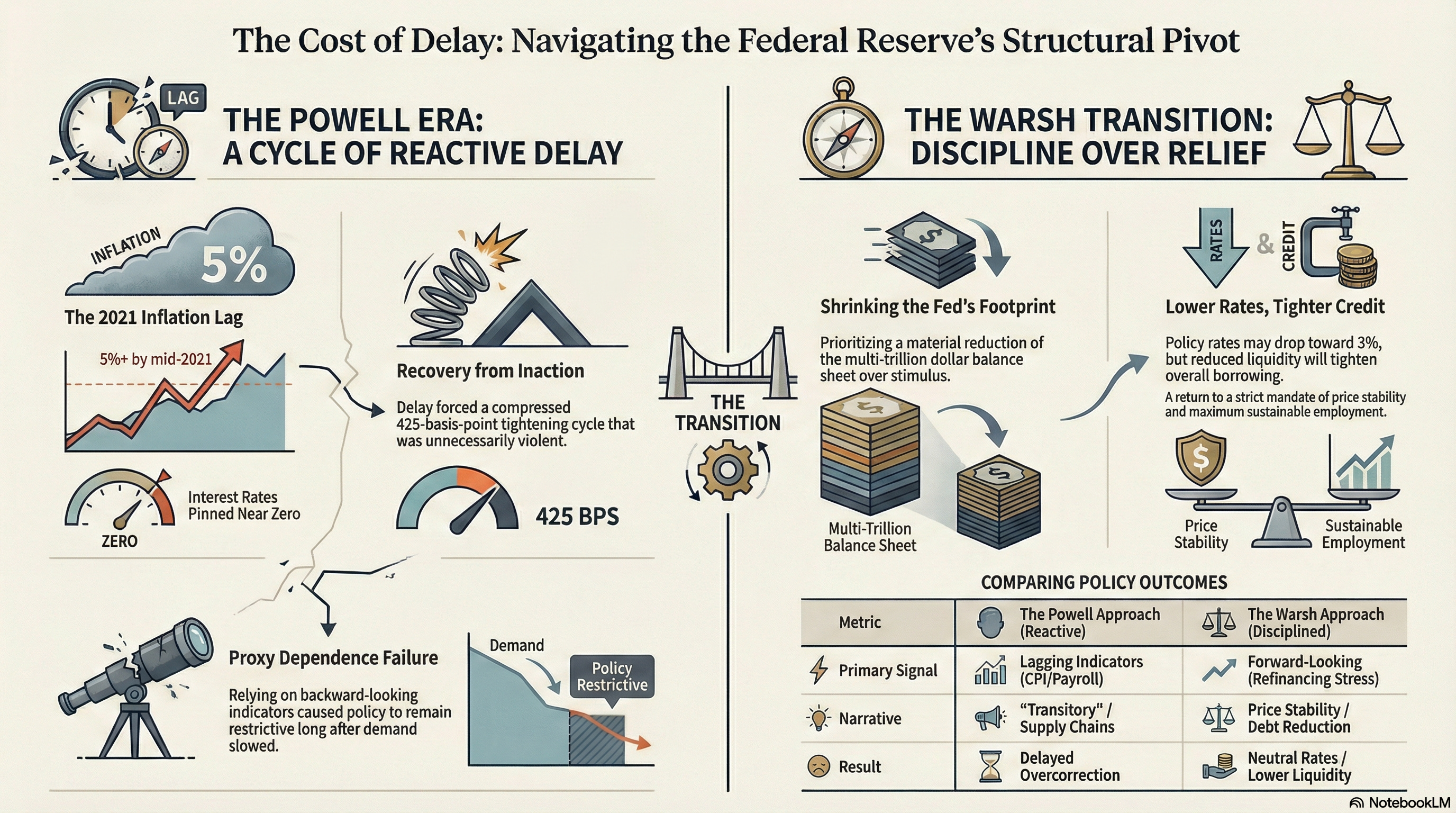

Inflation did not appear overnight. CPI climbed steadily through 2021, crossed 5 percent by mid year, and continued accelerating. Yet the policy rate remained pinned near zero until March 2022. By the time CPI peaked at 9.1 percent in June 2022, the Fed was already far behind the curve, not in hindsight, but relative to its own stated reaction function.

This delay forced a compressed tightening cycle that should never have been necessary. From December 2021 to December 2023, rates moved roughly 425 basis points, landing at a 5.25 percent to 5.5 percent target range by July 2023. That pace was not evidence of decisiveness, it was evidence of recovery from inaction.

Central banks rarely admit timing error directly, so they substitute narrative. The dominant narrative was transitory inflation, then supply chain normalization, then labor market resilience. Each narrative bought time. Each delayed adjustment. Each made the eventual adjustment more violent.

The result was predictable. When tightening is delayed, the only way to re-anchor expectations is through speed and severity. That severity does not distribute evenly. Rate sensitive sectors absorb it first. Housing, small business credit, venture financing, capital intensive manufacturing. None of those sectors drive headline CPI in real time, which creates the illusion that policy is not yet restrictive enough, reinforcing the error.

By mid 2023, the damage was already baked in. Mortgage rates moved into the 6 to 7 percent range. Commercial refinancing windows narrowed sharply. Credit availability tightened even as headline inflation began falling. Yet policy held steady.

That brings us to the second delay.

By 2025, the macro picture had changed materially. Real GDP grew at roughly 4 percent annualized in Q2. Unemployment sat near 4.1 percent. Inflation had cooled substantially from its peak. Financial conditions were restrictive by historical standards, not by Fed rhetoric, but by actual borrowing costs faced by households and firms. Despite this, rate cuts did not begin until September 2025.

The justification was caution. The stated risk was reigniting inflation. This is where precautionary principle thinking becomes a liability rather than a virtue. Precaution assumes asymmetric risk. In this case, the asymmetry ran the other way.

When inflation expectations are already anchored and demand is slowing under the surface, delay does not preserve stability. It quietly transfers stress into balance sheets that do not show up in CPI prints. It rewards cash holders and penalizes productive leverage. It increases default risk without delivering meaningful disinflation gains.

The deeper issue is proxy dependence. The Fed targets inflation, employment, and financial stability, but it operationalizes those goals through lagging indicators. CPI is backward looking. Payroll data is revised repeatedly. Financial stress only registers after credit breaks. When policymakers wait for confirmation in these proxies, they are always late.

This is not a moral failure. It is an incentive failure. Central bankers are punished more harshly for acting early and being wrong than for acting late and blaming data. Acting early risks visible error. Acting late diffuses responsibility into models and committees.

The Powell era illustrates this asymmetry cleanly. Early hikes in 2021 would have looked aggressive against prevailing narratives put forward by Janet Yellen and the Biden Administration. Gradual cuts in early 2025 would have looked risky against inflation trauma still fresh in institutional memory. In both cases, delay was safer for careers and reputations. In both cases, delay increased the real economic cost.

The lesson is not that central banks should abandon caution. It is that caution anchored to lagging proxies is indistinguishable from paralysis. If Keynesian economics is to be an effective methodology, then forward looking policy requires acting on the signals of credit growth deceleration, refinancing stress, and real rate compression. Not waiting for journalists or politicians to grant permission.

If inflation peaks at 9.1 percent and policy is still near zero, the problem is not a forecasting error. It is reaction delay. If GDP grows at 4 percent under restrictive rates and cuts are postponed another quarter, the problem is not prudence. It’s institutional inertia.

Powell’s legacy will likely be framed by that 9.1% inflationary number. The numbers suggest something even less flattering and more instructive. He was late when early action would have been cheaper. He was late when adjustment would have reduced hidden stress and allowed even faster growth. The costs were not evenly distributed, and they never are.

That is the real story. Not inflation. Not personalities. Timing, incentives, and the quiet damage caused by waiting for proxies to tell you what the system has already begun to feel.

What’s Next

Kevin Warsh is the nominee to succeed Jerome Powell as chair of the Federal Reserve, pending Senate confirmation. He is a former Fed governor who first served on the Board from 2006 to 2011, becoming one of the youngest members ever confirmed to that seat.

His academic credentials include degrees from Stanford and Harvard Law, and his early career blended roles in investment banking, government economic policy, and advisory work during the 2008 financial crisis.

President Trump has emphasized Warsh’s experience steering policy under duress and his alignment with a more market centric, inflation conscious view of the Fed’s mandate.

Some of his most public stances focus on shrinking the Fed’s balance sheet, tightening the institution’s focus to price stability and employment, and skepticism about extending the Fed’s reach into agenda areas beyond core monetary policy.

There is ongoing debate over how much his personal views will shape policy versus the collective stance of the Federal Open Market Committee, but his nomination signals a clear shift in leadership style and priorities relative to the last chair.

His stated agenda, as gleaned from public statements and commentary, centers on reining in the central bank’s footprint, reducing the balance sheet materially from its multi trillion dollar size, and advocating a return to strict focus on price stability and maximum sustainable employment.

He has also signaled openness to lower rates relative to Powell’s final stance, but market analysts caution that the FOMC’s consensus will constrain aggressive moves outside underlying economic fundamentals.

In practice, this suggests modest rate adjustments toward what many models consider a neutral real funds rate near 3 percent, rather than dramatic easing or tightening beyond that range.

If Warsh pushes down rates incrementally while also shrinking liquidity via balance sheet reduction, the net effect could be lower policy rates accompanied by tighter credit conditions in some sectors. This combination would be a nuanced pivot, not a wholesale regime change.

What does that mean for the fiscal future of America?

The Fed’s path under Warsh will feed directly into Treasury yields, budget financing costs, and the crowding effects of public debt.

Lower nominal rates reduce interest expense on new Treasury issuance and can compress yields across credit markets. At the same time, reducing the balance sheet shrinks the central bank’s demand for long duration assets, which could raise yields absent strong private demand. If nominal yields rise alongside lower policy rates, fiscal costs could increase, particularly in a regime of persistent federal deficits.

In practical terms, the path the Fed chooses affects the fiscal arithmetic of servicing debt, the valuation of long duration assets held by institutions and households, and the risk premiums embedded in corporate borrowing.

It also interacts with real economic growth through the cost of capital faced by firms and households. A Fed chair who pushes down short term rates without a commensurate easing of financial conditions overall can create a disconnect that tightens credit while superficially lowering policy costs.

What emerges from all of this is a cleaner and more uncomfortable truth. Monetary policy errors rarely look dramatic in real time, they look like patience, caution, and consensus.

The Powell years show how delay masquerades as prudence, first by forcing an unnecessarily violent tightening cycle, then by letting restrictive conditions linger long after the headline threat had passed.

The incoming chair does not signal a return to stimulus or a pivot toward growth at any cost. He signals a narrower, colder approach.

Lower policy rates paired with less liquidity. Discipline without relief. That regime has clear consequences. Capital flows toward strength, duration is repriced, leverage is exposed, and weak balance sheets stop being subsidized by time.

The winners and losers outlined below are not predictions in the narrative sense. They are mechanical outcomes of rates, term premia, and credit availability. If there is a bow to tie here, it’s this. In markets, timing is money, liquidity is power, and delay is never without cost.

Winners and Losers

Five Likely Public Market Winners

Large US banks and diversified financials, 70-80% confidence (up from 65-75%):

Keep reading with a 7-day free trial

Subscribe to Agora to keep reading this post and get 7 days of free access to the full post archives.